Can You Really Buy $1 for 80 Cents?

A few years ago, I was sitting in a small coffee shop with an older friend named David.

A few years ago, I was sitting in a small coffee shop with an older friend named David.

David is the kind of man who still reads the newspaper in print.

He folds the pages carefully. Brings his own pen. And somehow always ends up doing math on napkins.

He worked for more than forty years. Saved consistently. Avoided debt. Never chased trendy investments.

“I don’t need excitement anymore,” he once told me.

“I need income.”

That morning he was stirring his coffee slowly and staring at his phone calculator with the kind of expression people make when reality starts becoming expensive.

“They raised my savings account again,” he said.

“Oh?”

“Almost 2% now.”

He gave a dry little laugh.

Not the happy kind.

The tired kind.

Then he looked up at me.

“Inflation is what now? Three percent? Four?”

“Something like that.”

David nodded slowly.

“So I’m still losing money safely.”

That sentence stayed with me.

Losing money safely.

Because that’s exactly how many people feel right now.

They did everything responsibly. Worked hard. Saved carefully.

And somehow the numbers still feel backwards.

A few minutes later, I asked him a strange question.

“David… if somebody offered you a $100 gift card for $80… would you buy it?”

He looked at me like I had insulted his intelligence.

“Of course.”

“What if they offered ten of them?”

“I’d buy all ten.”

“What if the store owner said:

‘People just don’t really like gift cards right now.’”

David laughed.

“That would be ridiculous.”

And that’s when I told him:

“The stock market does something very similar all the time.”

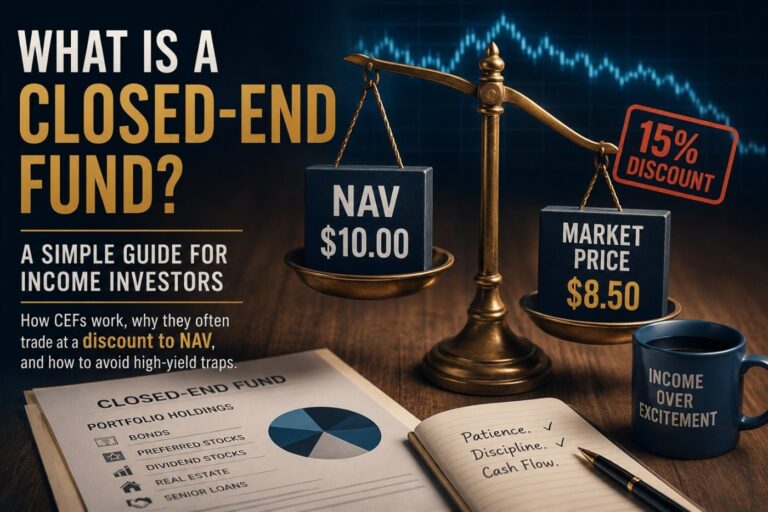

There’s a strange little corner of investing called closed-end funds.

Most people have never heard of them.

Which is funny, because some of them are older than the highways we drive on.

A closed-end fund — usually called a CEF — is basically just a basket of investments.

Sometimes bonds. Sometimes dividend stocks. Sometimes real estate loans.

The fund collects income from those investments and pays it out to shareholders.

Pretty simple.

But here’s where things get strange.

Imagine the investments inside the fund are worth $10 per share.

Not theoretically worth $10.

Actually worth $10.

If you sold everything inside the fund today, you’d roughly end up with $10 per share.

Wall Street has a fancy name for this:

NAV.

Net Asset Value.

Which is really just a complicated way of saying:

“What’s all the stuff inside actually worth?”

But sometimes the market looks at that $10 worth of assets and says:

“Eh… I’ll give you $8 for it.”

David stopped stirring his coffee.

“Wait,” he said.

“They know it’s worth ten?”

“Yes.”

“And they still sell it for eight?”

“Sometimes.”

He leaned back in his chair.

“Huh.”

That’s usually the moment people become interested in CEFs.

Not because they sound exciting.

But because they sound oddly sensible.

And yes — this really happens.

The chart below shows a real closed-end fund called FS Credit Opportunities Corp. (FSCO), where the market price fell far below the actual value of the assets inside the fund.

The blue line shows what the portfolio itself was worth.

The dark line shows what emotional human beings were willing to pay for it.

Sometimes the gap becomes surprisingly large.

Especially when fear enters the market.

The obvious question, of course, is this:

Why would anyone do that?

Because markets are not machines.

They’re crowds.

And crowds are emotional.

Sometimes investors get scared. Sometimes interest rates rise. Sometimes entire categories of investments become unpopular for years at a time.

And when that happens, people stop caring what something is worth.

They just want out.

Strange things happen when human emotion gets attached to money.

Perfectly decent assets become unloved.

Not broken.

Just unfashionable.

It’s a little like winter coats going on clearance in February.

The coats still work perfectly fine.

People are simply tired of winter.

The strange thing is that markets sometimes do the opposite too.

Sometimes investors become so enthusiastic about a fund that they willingly pay MORE than the underlying assets are actually worth.

The chart below shows a real example: Cornerstone Strategic Value Fund (CLM), where investors consistently paid a premium simply because the fund became popular.

Same market.

Same human psychology.

Different emotion.

Wall Street usually prefers exciting stories.

Artificial intelligence. Disruption. The next trillion-dollar revolution.

A boring bond fund quietly paying monthly income is much harder to market.

Which may be exactly why opportunities sometimes survive there.

Because boring things are often ignored.

And ignored things are sometimes mispriced.

At this point David pulled his napkin closer and started writing numbers on it.

“So let me get this straight,” he said.

“If the fund owns ten dollars worth of investments…”

“Right.”

“And I buy it for eight…”

“Right.”

“Then I’m collecting income from ten dollars worth of assets while only spending eight?”

“In simple terms… yes.”

David stared at the napkin for a moment.

Then he shook his head and laughed.

“The market really is strange.”

It is.

Especially when fear enters the picture.

Because when investors panic, discounts can become even larger.

People stop asking:

“What is this worth?”

And start asking:

“How fast can I sell it?”

That’s when calm investors sometimes find opportunity.

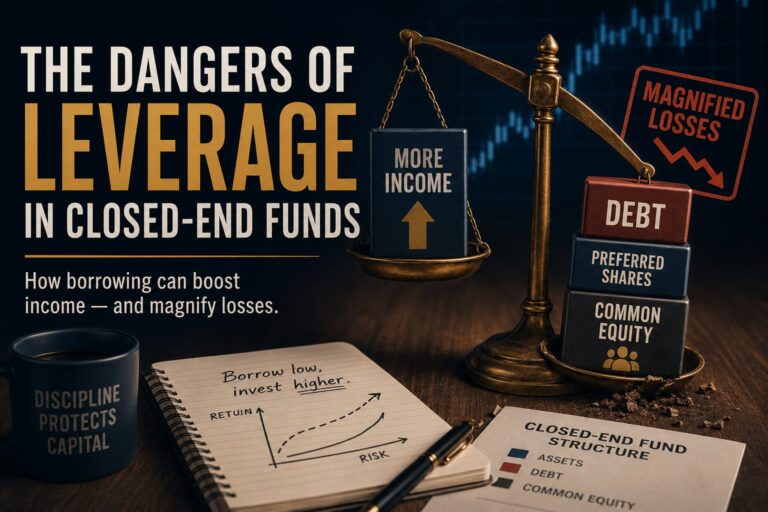

Now before this starts sounding too magical, we should probably add the warning label.

Because discounts are not free money.

Some CEFs use leverage — borrowed money — to increase returns.

Which works beautifully…

…until it doesn’t.

Leverage is a little like putting a motorcycle engine on a bicycle.

Everything becomes faster.

Including the crashes.

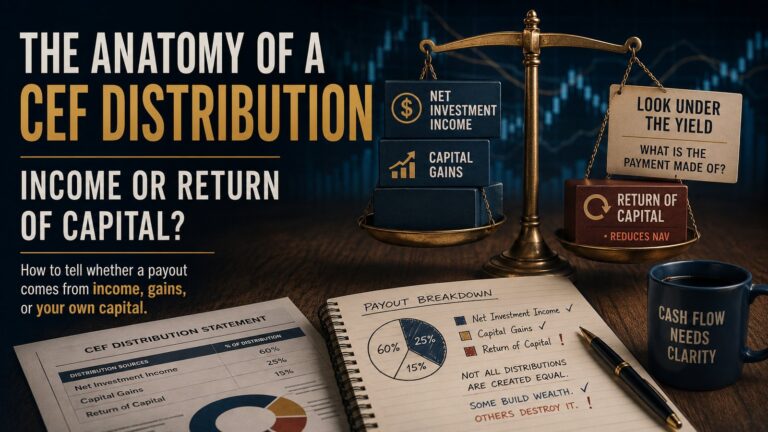

Some funds also advertise giant yields that look wonderful right before they collapse.

And some slowly hand investors their own money back while pretending it’s “income.”

So yes:

discounts matter.

But quality matters too.

A cheap thing is not automatically a good thing.

A rotten apple sold at half price is still a rotten apple.

This is where things become interesting.

Some funds trade below the value of their assets.

Others trade above it.

Here’s a simple real-world snapshot:

FSCO was trading below the value of its underlying assets.

CLM was trading above them.

Same market.

Same emotional humans.

Very different behavior.

David nodded at that.

“That,” he said,

“sounds more like Wall Street.”

Still, there’s something deeply fascinating about the whole idea.

Because closed-end funds quietly reveal a truth most people never hear about markets.

Prices and value are not always the same thing.

Sometimes people become fearful. Sometimes impatient. Sometimes irrational.

And every once in a while, that emotional behavior creates an opportunity for calmer investors.

Not a lottery ticket.

Not a “get rich quick” scheme.

Just the simple opportunity to buy good cash-flow-producing assets a little cheaper than you probably should be able to.

David folded the coffee receipt and slipped it into his wallet.

Then he smiled.

“Funny,” he said.

“I spent my whole life looking for bargains.”

He paused.

“Never occurred to me the stock market might have clearance aisles too.”