What Is a Closed-End Fund? A Simple Guide for Income Investors

Closed-end funds can trade below the value of their assets and pay regular income, but high yields and discounts require careful analysis.

Most investors eventually reach the same quiet question.

Not at the beginning, when investing still feels exciting. Not when they are watching stock charts, reading headlines, or calculating how much the S&P 500 returned last year. It usually happens later, when life has become more expensive, the account balance has grown a little, and the investor starts thinking less about excitement and more about cash flow.

“How do I make this portfolio actually pay me?”

That is where income investing begins to feel less like a strategy and more like a need.

Dividend stocks are one answer. Bonds are another. Real estate can be another, although it comes with tenants, repairs, taxes and the occasional leaking roof. But there is a quieter corner of the market that many ordinary investors never really study: Closed-End Funds, usually called CEFs.

They are not magic. They are not risk-free. And they are definitely not something to buy just because the yield looks high.

But for a patient income investor, they are worth understanding.

The Strange Little World of Closed-End Funds

A Closed-End Fund is an investment fund with a fixed number of shares.

That one sentence explains almost everything important about CEFs.

A regular mutual fund grows and shrinks as investors put money in or take money out. When new investors arrive, new fund shares are created. When investors leave, shares are redeemed. The fund expands and contracts with investor demand.

ETFs are different in the details, but they also have a creation and redemption mechanism that helps keep the market price close to the value of the assets inside the fund.

A Closed-End Fund does not work that way.

A CEF usually raises money once, through an initial public offering. The fund manager then takes that pool of capital and buys investments: bonds, preferred stocks, dividend-paying companies, real estate securities, senior loans, municipal bonds or other income-producing assets.

After that, the fund’s shares trade on the stock exchange. If you want to buy into the fund, you buy shares from another investor. If you want to sell, another investor has to buy them from you.

The fund itself is “closed.” The number of shares is generally fixed.

That small structural difference creates something unusual. The value of the assets inside the fund and the price of the fund’s shares can move apart.

And that is where CEFs become interesting.

What Is NAV?

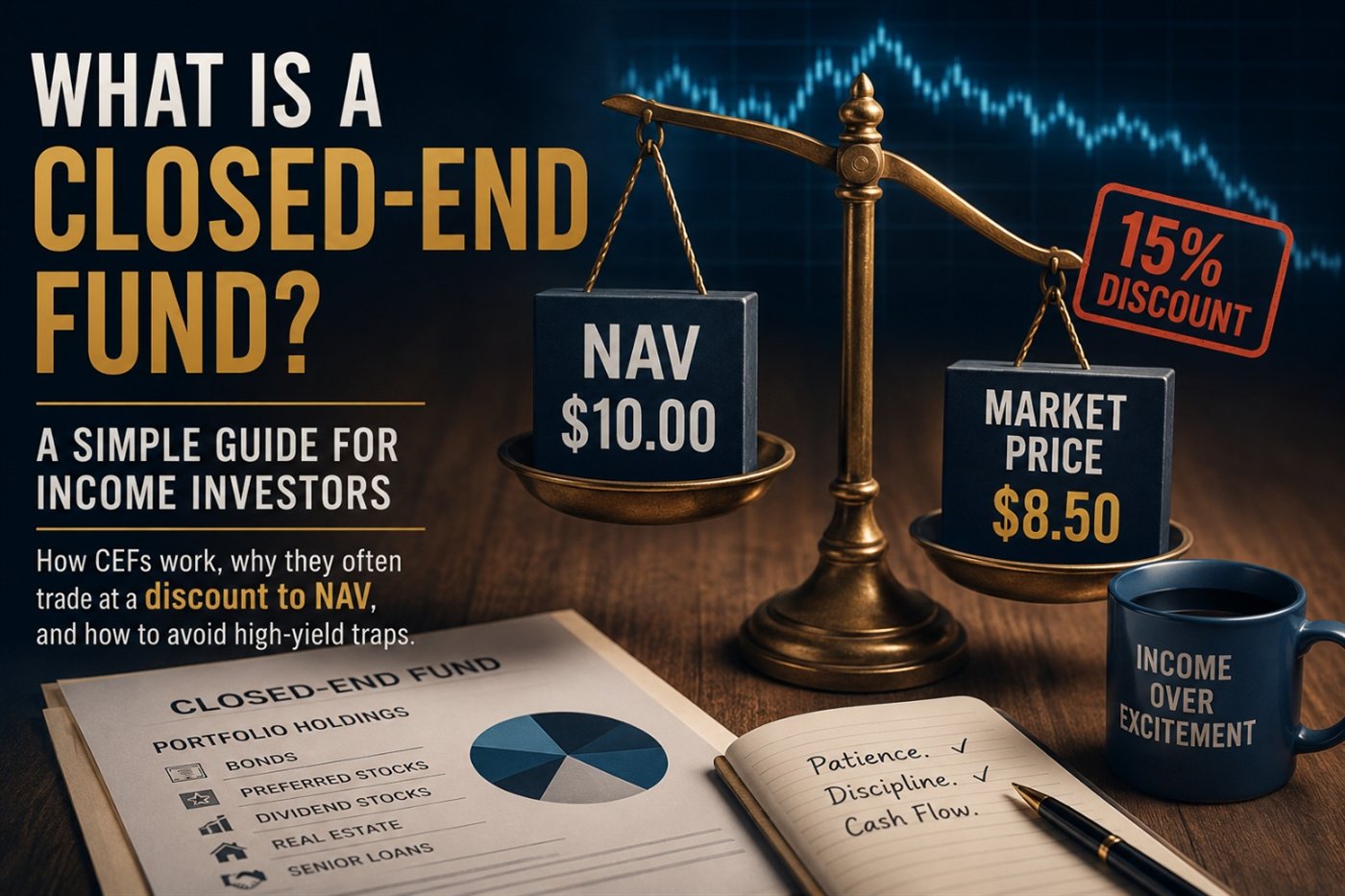

NAV stands for Net Asset Value.

It is the estimated value of everything inside the fund, divided by the number of shares. In plain English, NAV answers a simple question:

What is the stuff inside the fund actually worth?

Imagine a CEF owns a portfolio of corporate bonds. If all those bonds together are worth $100 million, and the fund has 10 million shares, the NAV is $10 per share.

That does not mean investors will pay $10 for the shares.

They might pay $9.

They might pay $11.

Sometimes, especially when investors become fearful, they might pay much less.

That gap between the fund’s NAV and its market price is one of the main reasons income investors study Closed-End Funds.

Buying Income Below Its Stated Value

Let’s keep the numbers simple.

A CEF has a NAV of $10 per share. That means the investments inside the fund are estimated to be worth $10 per share. But on the stock exchange, the shares trade for $8.50.

That fund is trading at a 15% discount to NAV.

In ordinary language, you are buying $10 of underlying assets for $8.50.

That sounds attractive, and sometimes it is. But it is not automatic free money. The assets inside the fund may fall in value. The discount may become even wider. The fund may use too much leverage. The distribution may later be cut.

Still, the idea is powerful.

If the assets inside the fund produce income, and you buy those assets below their stated value, your personal income yield can become higher than the yield on the fund’s NAV. The income generated by the assets does not change simply because you bought the fund at a discount. What changes is the price you paid to receive that income.

That is why some income investors like CEFs. They are not just looking for yield. They are looking for yield purchased at a sensible price.

There is a big difference.

Do CEFs Really Trade at Discounts?

Yes. Discounts are not just a theoretical curiosity.

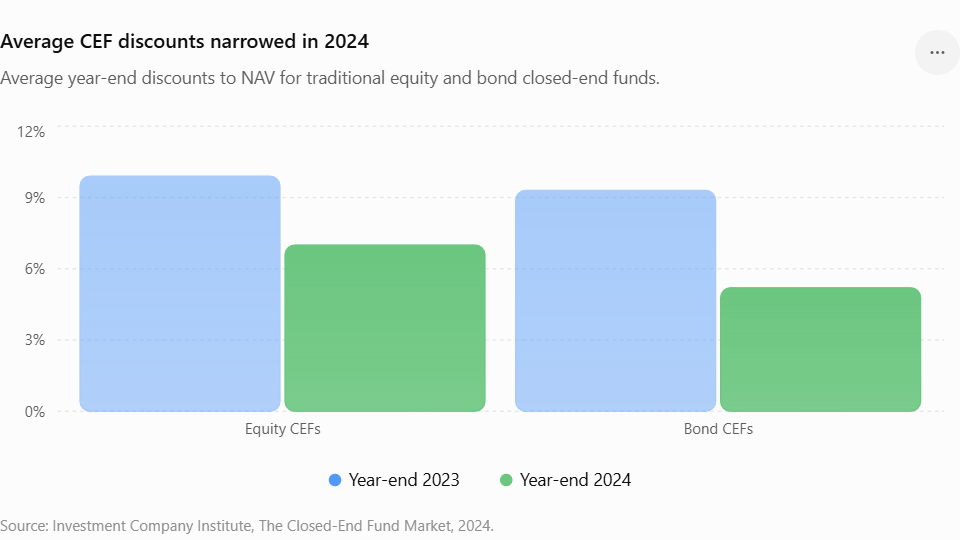

The Investment Company Institute reported that traditional CEF discounts narrowed in 2024. Equity CEF discounts moved from 9.9% at year-end 2023 to 7.0% at year-end 2024. Bond CEF discounts moved from 9.3% to 5.2% over the same period.

That does not mean every CEF was cheap. It does not mean every discount was attractive. But it does show something important: discounts are a normal and measurable feature of the closed-end fund market.

The lesson is simple.

In the CEF world, price and value often travel together, but they do not walk in perfect step.

Why Do Closed-End Funds Trade at Discounts?

Markets are not machines. They are crowds.

And crowds are often emotional.

When investors become nervous, they sell. When interest rates rise, they sell. When a fund cuts its distribution, they sell. When a sector becomes unpopular, they sell. Sometimes they sell because they understand the risk. Sometimes they sell because they are tired of seeing red numbers on a screen.

Because CEF shares trade on the open market, that selling pressure can push the share price below the value of the assets inside the fund.

This can create opportunity for calm investors.

But only if the assets are still sound.

That distinction matters. An unloved fund can be interesting. A damaged fund can be dangerous. The job of the income investor is to tell the difference.

Why Do CEFs Often Pay High Income?

When investors first discover Closed-End Funds, they often notice the yields.

Seven percent. Nine percent. Sometimes even more.

Compared with a broad index fund, those numbers can look suspicious. And to be fair, sometimes they are. A very high yield should slow you down, not speed you up.

But CEFs often pay more because many of them are built specifically for income. They may hold bonds, preferred shares, loans, real estate securities or dividend-focused assets. Their goal is often not to become the next exciting growth story. Their goal is to collect income and distribute it to shareholders.

There are three common engines behind CEF income.

The first is ordinary income. Bonds pay interest. Preferred stocks pay dividends. Loans pay interest. The fund collects that cash, subtracts expenses, and distributes the remaining income to investors.

The second is leverage. Many CEFs borrow money to buy more income-producing assets. If a fund can borrow at a lower rate than it earns on the assets it buys, the difference can increase shareholder income.

That sounds nice, and in calm markets it can work beautifully.

But leverage is a tool, not a miracle. It can increase income, but it can also increase volatility. When interest rates rise, credit spreads widen or markets fall, leverage makes everything move faster. Including the losses.

The third source is Return of Capital, often called ROC. This means part of the distribution is not ordinary income. Sometimes ROC is harmless or even tax-efficient. But sometimes it means the fund is handing investors their own money back while presenting it as income.

That is where yield traps begin.

The Yield Trap

A yield trap is a fund that looks attractive because the payout is high, while the underlying economics are weak.

This is one of the biggest risks with Closed-End Funds.

Imagine a fund paying 13%. That looks wonderful on a screen. It looks like income. It looks like progress. It looks like the portfolio is finally working for you.

But behind the scenes, the fund may not be earning enough to support that payout. It may be using Return of Capital in a destructive way. It may be selling assets to maintain the distribution. It may be watching its NAV decline year after year.

For a while, the investor feels rewarded. The monthly payment arrives. The yield looks impressive. The portfolio appears productive.

Then the distribution is cut.

The share price falls. The income falls. And suddenly the high yield was not a gift. It was a warning label.

Four Things to Check Before Buying a CEF

You do not need to become a Wall Street analyst to understand the basics of a CEF. But you do need to slow down and ask a few simple questions.

First, look at the discount or premium. Is the fund trading below NAV or above NAV? More importantly, how does the current discount compare with its own history? A fund that always trades at a 12% discount may not be unusually cheap. A fund that normally trades at a 5% discount but now trades at 15% might deserve a closer look.

Second, study the distribution history. Has the fund maintained its payout over time, or has it repeatedly cut the distribution? A single cut is not always bad. Sometimes it is responsible. But a long history of cuts tells you something about the fund’s ability to support its promises.

Third, look at NAV over time. This may be the most important habit. A fund that pays 10% but loses 12% of NAV every year is not creating wealth. It is slowly giving you your own money back.

Fourth, understand leverage. A fund that borrows money can produce higher income, but it can also become more fragile when borrowing costs rise or markets fall. Leverage is not automatically bad, but it should never be invisible to you.

Where to Find CEF Data

The basic data for Closed-End Funds is not difficult to find, but it does require a little effort.

CEFConnect and the Closed-End Fund Association are useful starting points for basic CEF data. They can help you compare discounts, premiums, asset classes, distributions and leverage.

Broker platforms may also help you screen funds by income, asset type, market price and valuation. The important thing is not the excitement of trading. It is the discipline of comparing funds before putting real money at risk.

For deeper research, many income investors also read fund reports, manager commentary and investor analysis. Not every opinion will be right. But reading different arguments can help you notice risks you might otherwise miss.

The goal is simple.

Do enough work so that you are not buying a fund merely because the yield looked good on a lazy afternoon.

Are CEFs Right for Every Investor?

No.

Closed-End Funds are not savings accounts. They are not simple index funds. They are not guaranteed income machines.

They can fall in price. They can use leverage. They can cut distributions. Their discounts can get wider. Their underlying assets can lose value. And the investor who buys only because of a large yield may end up learning an expensive lesson.

But CEFs can be useful for the right kind of investor.

They may offer diversified income, professional management, monthly or regular distributions, and the possibility of buying income-producing assets below their stated value. For investors building a cash-flow portfolio, that can be attractive.

The key is temperament.

A CEF investor needs patience. Not blind patience, but informed patience. The kind that understands the difference between volatility and permanent damage. The kind that can look at a discount and ask, calmly:

“Is this fear, or is this a real problem?”

That question matters more than the yield.

Research Behind This Article

This article is written for ordinary income investors, but the closed-end fund puzzle has been studied seriously in academic finance for decades.

The main idea is simple: a CEF’s market price can differ from the value of the assets inside the fund. Researchers have connected that gap to investor sentiment, management fees, liquidity, tax effects, leverage and the practical limits of arbitrage.

The practical lesson for investors is not that every discount is a bargain.

The lesson is that price and value can separate, and the patient investor must understand why before acting.

The Bottom Line

Closed-End Funds are one of the more interesting corners of income investing.

Their structure creates a simple but powerful possibility: the market price of the fund can trade below the value of the assets inside it. Sometimes that creates opportunity. Sometimes it exposes risk. The difference depends on the quality of the assets, the sustainability of the distribution, the use of leverage and the behavior of investors.

A calm income investor does not chase the biggest number on the screen.

He asks better questions.

What does the fund own?

What is the NAV?

Is the discount unusual?

Is the payout covered?

Is leverage helping or hurting?

Is this durable income, or just a high yield wearing a nice suit?

That is the real work.

Because in the end, income investing is not about finding the loudest yield.

It is about building cash flow you can understand.

And understanding is still one of the most underrated forms of risk management.