How to Find and Screen Closed-End Funds Without Chasing Yield

It usually happens late at night, with a cup of coffee nearby and too many browser tabs open. The investor discovers a Closed-End Fund screener, clicks “sort by yield,” and suddenly the screen fills with beautiful numbers.

There is a dangerous moment in every income investor’s research.

It usually happens late at night, with a cup of coffee nearby and too many browser tabs open. The investor discovers a Closed-End Fund screener, clicks “sort by yield,” and suddenly the screen fills with beautiful numbers.

Nine percent. Eleven percent. Thirteen percent.

For a moment, it feels like a secret door has opened. The portfolio in his mind starts paying the mortgage, the groceries, the electricity bill, maybe even a little freedom. It feels like discovery.

But sometimes it is only temptation wearing a spreadsheet.

Closed-End Funds are wonderful to research because the data is visible. You can see the market price, NAV, discount, premium, distribution rate, leverage, asset class and performance history. But visible data is not the same as understanding.

A screener can help you find candidates.

It cannot tell you what to buy.

That part still belongs to judgment.

Start With the Right Question

Most beginners start with the wrong question.

They ask:

“Which CEF has the highest yield?”

That sounds reasonable, but it is usually where the trouble begins. A high yield may be attractive, but it may also be a warning sign. The fund may be using too much leverage, paying more than it earns, returning capital destructively, or watching its NAV decline year after year.

A better question is:

“Which CEF has durable income, reasonable valuation and risks I can understand?”

That question changes the whole research process. Instead of sorting only by yield, you begin with structure. You look at the asset class, NAV history, discount history, distribution record, leverage, expenses and fund documents.

You are not hunting for the loudest number.

You are trying to find a fund whose income makes sense.

Where to Find CEF Data

There are several useful places to begin.

CEFConnect is one of the most common free tools for CEF investors. It can be useful for checking daily pricing, NAV, market price, fund details, distribution information, portfolio tools and alerts.

CEF Channel is helpful for quick screening. It organizes CEFs by categories and provides screens for things like biggest discount to NAV, biggest premium to NAV, highest dividend yield, highest yield on NAV and trailing performance.

The Closed-End Fund Association is useful when you want to understand the language of CEFs rather than simply chase tickers. It provides educational material, fund selection information, performance history concepts, premium and discount reports and general CEF basics.

Fund sponsor websites are also important. If you are researching a specific fund, the sponsor’s own documents usually matter most. Look for the fact sheet, annual report, semi-annual report, distribution notices, leverage information, portfolio holdings and expense details.

Broker platforms can help too, especially when you want to compare market prices, build watchlists or track funds over time. Investor research platforms and articles can also be useful, not because every opinion is correct, but because they may point you toward risks you had not noticed.

The FireByMike CEF Screening Framework

If you want to research Closed-End Funds without drowning in data, use a calm order. Start with what the fund owns, then look at valuation, then examine the distribution, NAV trend, leverage and documents.

Do not begin with the yield.

End with the yield.

1. Asset Class What does the fund actually own: municipal bonds, corporate credit, preferred stocks, covered calls, REITs, senior loans, or something else?

2. Discount or Premium Is the fund trading below NAV or above it?

3. Discount History Is today’s discount unusually wide, or is this normal for the fund?

4. Market Yield vs NAV Yield What do you receive based on market price, and what must the fund earn on NAV to support the payout?

5. Distribution History Has the fund maintained, grown, or repeatedly cut its payout?

6. NAV Trend Is the underlying asset base stable, or is the fund slowly shrinking?

7. Leverage How much borrowing is used, and what risks does that create?

8. Expenses Are fees and leverage costs reasonable for the strategy?

9. Sponsor Documents Read the fact sheet, annual report, holdings, distribution notices and leverage information.

10. Watchlist Before Buy List Track the fund first. A watchlist is where good ideas prove themselves before real money gets involved.

That framework will not choose a fund for you. But it will help you avoid the most common beginner mistake: starting with yield instead of structure.

Asset Class Comes First

A CEF is only a wrapper.

What matters first is what sits inside the wrapper.

A municipal bond CEF is not the same as a high-yield bond CEF. A covered-call equity fund is not the same as a preferred stock fund. A real estate CEF is not the same as a senior loan fund.

Before comparing yields, decide what kind of exposure you actually want. Do you want municipal bonds, corporate credit, preferred stocks, covered calls, utilities, real estate, senior loans, emerging market debt or dividend equities?

Each asset class has its own risks. Interest-rate risk, credit risk, equity risk, currency risk and liquidity risk are not interchangeable.

A high-yield bond fund and a municipal bond fund may both pay monthly distributions, but they are not doing the same job.

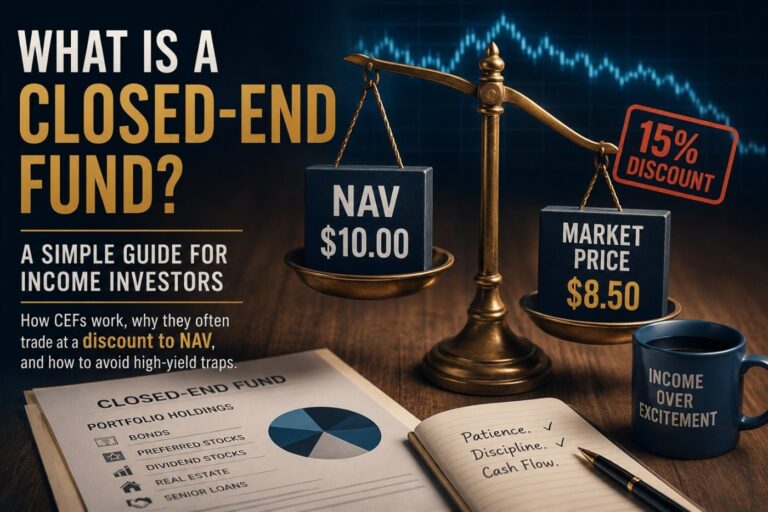

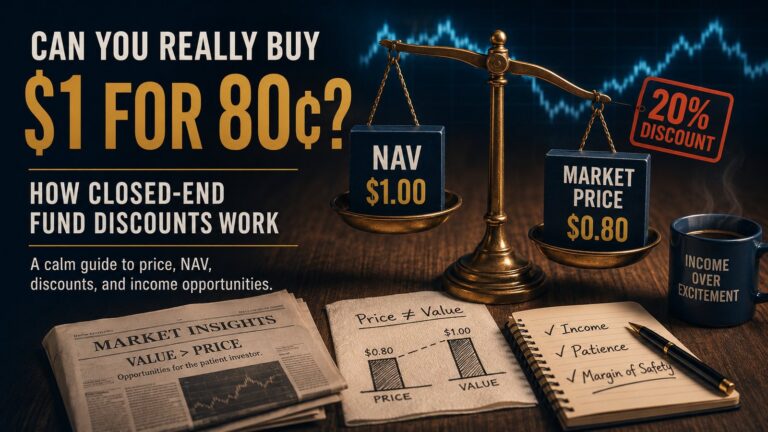

Discount Is Not Enough

After asset class, look at the discount or premium to NAV.

A discount means the fund’s market price is below the value of the assets inside the fund. A premium means the market price is above NAV. This is one of the most important features of CEF investing, but also one of the most misunderstood.

A fund trading at a 12% discount is not automatically cheap. It may always trade at a 12% discount. Or it may deserve that discount because of poor performance, high fees, weak distribution coverage, excessive leverage or a strategy investors no longer trust.

The better question is:

“How does today’s discount compare with this fund’s own history?”

A fund that normally trades near NAV but suddenly trades at a 12% discount may deserve attention. A fund that has traded at a deep discount for years may be telling you something else.

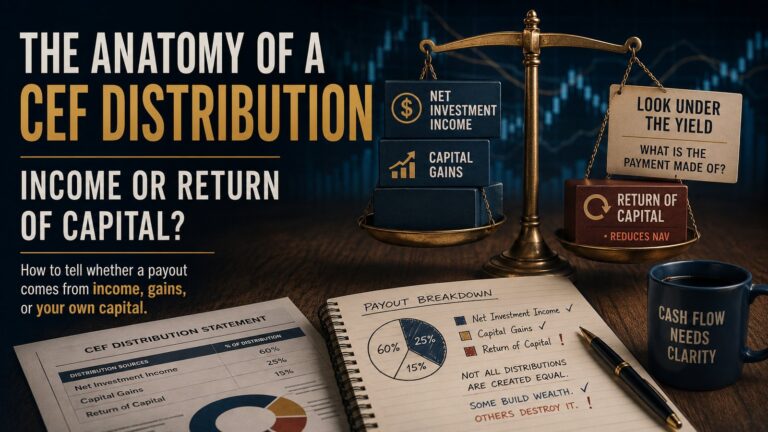

Market Yield Versus NAV Yield

Many screeners show the distribution rate based on market price. That number tells you what you receive based on the price you pay.

But you should also look at yield on NAV.

Yield on NAV tells you what the fund must generate on its underlying asset base to support the payout. This distinction matters because a fund trading at a discount may show a higher market yield than NAV yield.

For example, if a fund has a NAV of $10 and pays $0.80 per year, its NAV yield is 8%. If the same fund trades at $8, the market yield is 10%. The investor receives a higher yield on the price paid, but the fund still only has to support the distribution from the assets inside the fund.

That can be attractive.

But if a fund has a very high yield on NAV, the question becomes much harder: how exactly is the fund generating that payout?

Through bond income? Leverage? Capital gains? Options? Return of Capital?

The screen gives you the number. You still have to understand the source.

NAV Is the Quiet Witness

A fund can keep paying distributions while its market price moves around emotionally. But NAV shows what is happening to the underlying asset base.

If NAV is reasonably stable across a full market cycle, that is encouraging. It does not prove that the fund is safe, but it suggests that the fund is not simply destroying its own foundation to maintain the distribution.

If NAV steadily declines while the fund keeps paying a large distribution, the income may be less durable than it appears. The fund may be paying shareholders while slowly shrinking the asset base that supports future payments.

A high distribution with a falling NAV is not automatically a disaster.

But it demands an explanation.

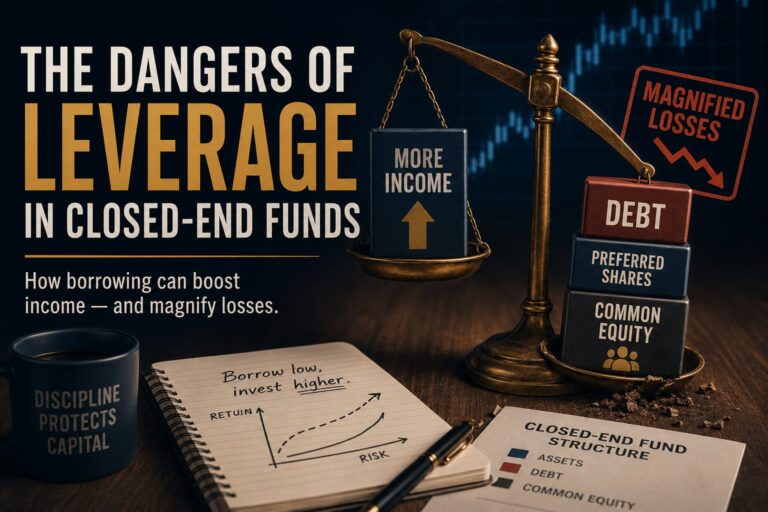

Leverage Can Change the Whole Picture

Leverage is one of the most important CEF screening factors.

A leveraged fund can pay more income because it owns more assets than it could own with shareholder capital alone. But leverage also increases sensitivity to market declines, credit stress and borrowing costs.

When screening, look for the leverage ratio. Then ask what kind of assets the fund is leveraging. Leverage on high-quality bonds is very different from leverage on volatile credit, emerging market debt or equity strategies.

Also consider the cost of leverage. A fund that looked comfortable when short-term rates were low may be less comfortable when borrowing becomes expensive.

Read the Sponsor Documents

Screeners are useful, but they are not the final source.

Once a fund interests you, go to the fund sponsor’s website. Read the fact sheet. Look at the annual report. Check the semi-annual report. Review the distribution notices, portfolio holdings and leverage information.

You are looking for simple things. What does the fund own? How much leverage does it use? What are the expenses? What is the distribution policy? What risks does the sponsor itself disclose?

If the sponsor documents are confusing, incomplete or hard to reconcile with the attractive yield, slow down.

Confusion is not a margin of safety.

Quick Red Flags

Some funds deserve extra caution before they deserve your capital.

Quick Red Flags Be careful when a fund combines several of these warning signs:

Very high market yield The payout looks attractive, but may not be sustainable.

Very high NAV yield The fund may need unusually strong returns to support the distribution.

Falling NAV The underlying asset base may be shrinking over time.

Repeated distribution cuts The payout may have been too ambitious in the past.

High leverage Borrowing can boost income, but it can also magnify losses.

High expenses Fees and borrowing costs reduce what belongs to shareholders.

Persistent premium Paying above NAV can make even a good income stream less attractive.

Unclear strategy If you cannot explain what the fund owns and how it pays you, slow down.

Any one of these may be explainable. Together, they deserve caution.

Also be careful with funds trading at large premiums. A premium means you are paying more than the stated value of the assets inside the fund. Sometimes investors are willing to do this because they love the distribution, the manager or the strategy. But paying too much for income can quietly reduce future returns.

A good income stream can still be a bad purchase if the price is wrong.

Build a Watchlist, Not a Shopping Cart

This is where discipline matters.

When you find a fund that looks interesting, do not immediately treat it as a buy. Put it on a watchlist. Track the discount, NAV, distribution, leverage and market price for a while.

A watchlist gives you time to think.

It also helps you avoid the emotional rush of discovering a high yield. Many bad purchases happen because the investor feels that an opportunity must be captured immediately. But most CEFs are not disappearing tomorrow.

Patience is part of the research process.

A Practical Example of the Thought Process

Imagine a CEF screener shows a fund yielding 11% at a 13% discount to NAV.

At first glance, that looks attractive.

But the calm investor does not stop there. He checks the asset class and sees that the fund owns lower-quality credit. He checks leverage and finds that it borrows heavily. He checks NAV and sees a steady decline over several years. He checks the distribution history and finds multiple cuts. He checks yield on NAV and realizes the fund must generate a very high return on its assets to keep paying.

Now the picture changes.

The 11% yield is no longer simply attractive. It is a question mark.

That does not automatically mean the fund is uninvestable. But it means the investor has moved from excitement to investigation.

That is progress.

The Bottom Line

CEF screeners are powerful.

They can show you discounts, premiums, yields, NAVs, performance, leverage and asset classes in seconds. But they can also tempt you into thinking that the highest yield is the best opportunity.

It usually is not.

The best CEF research begins with patience. You are not looking for the biggest number. You are looking for an income stream that you can understand, a valuation that makes sense, and risks you are willing to own.

A good screener helps you build a watchlist.

A good investor knows what to remove from it.

That is the difference.

In income investing, the goal is not to be impressed by the screen. The goal is to build cash flow without lying to yourself.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. Investing involves risk, including the possible loss of principal. Always do your own research or consult a qualified financial professional before making investment decisions.