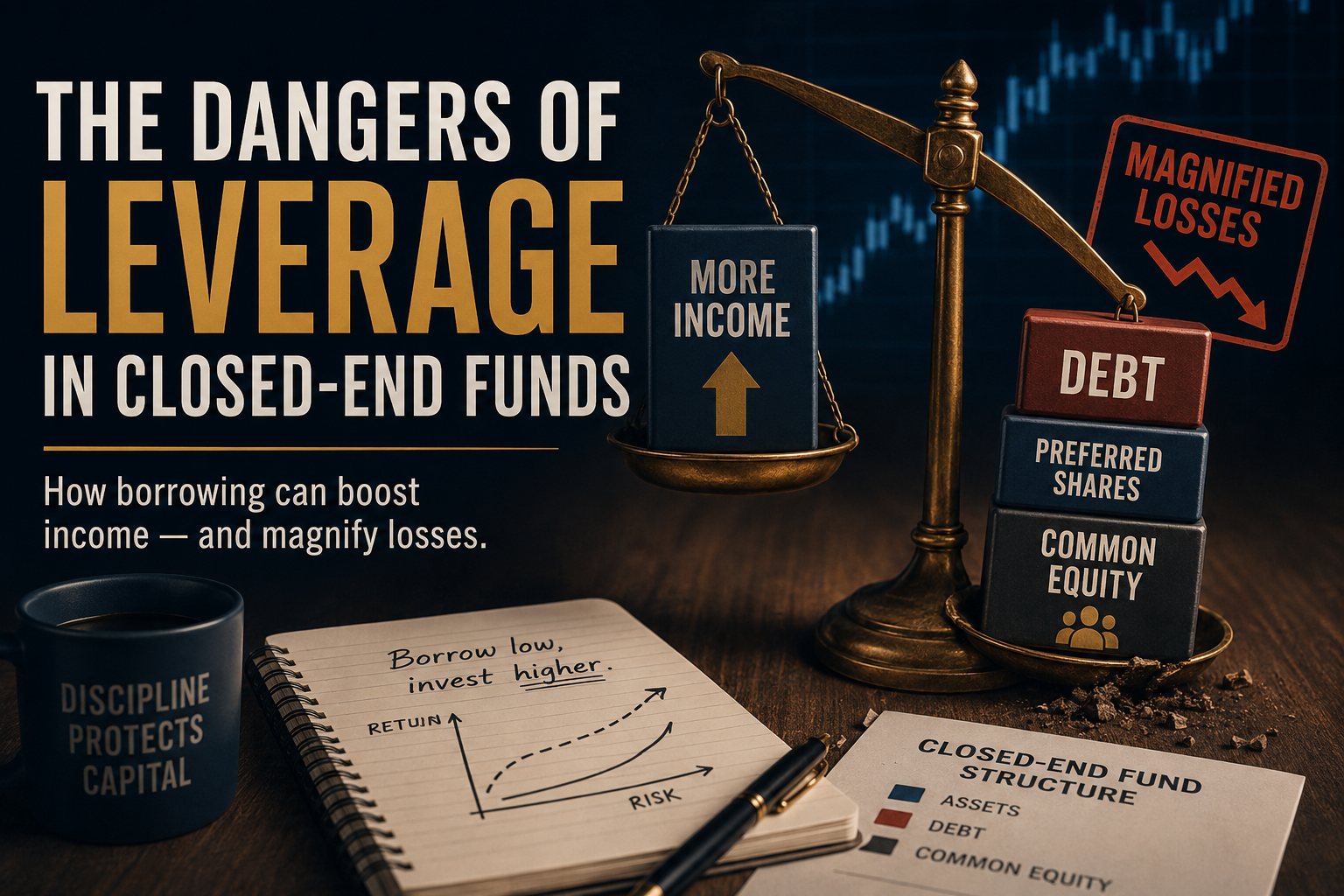

The Dangers of Leverage in Closed-End Funds

There is a sentence that sounds harmless until real money is attached to it.

There is a sentence that sounds harmless until real money is attached to it.

“We can borrow a little.”

At the kitchen table, that sentence might mean a renovation, a car, or a bigger house than the family originally planned. In investing, it often means something more technical, but the emotional logic is not so different. Borrowing makes a plan feel larger. It pulls the future forward. It gives ordinary numbers a little more muscle.

Closed-End Funds use that same idea.

Many CEFs borrow money so they can buy more income-producing assets. If the fund owns bonds, preferred stocks, senior loans, real estate securities or dividend-paying companies, leverage allows the manager to own more than the fund could buy with shareholder capital alone. That can increase income. It can also increase pain.

This is why leverage deserves its own calm explanation.

What Leverage Means in a CEF

A Closed-End Fund usually raises a fixed pool of capital and invests that money. But many CEFs do not stop there. They borrow additional money and use it to buy more assets.

The basic idea is simple. If a fund can borrow at 4% and invest the borrowed money into assets yielding 7%, the extra spread can benefit shareholders. That spread helps explain why some CEFs can pay distributions that look much higher than ordinary bond funds or broad market ETFs.

That is the attractive side of leverage: it turns a normal income engine into a larger one. But if borrowing costs rise, asset prices fall, credit spreads widen, or the fund is forced to reduce leverage at a bad time, the same tool that helped the income stream can begin to work against the shareholder.

Why Closed-End Funds Use Leverage

Closed-End Funds are structurally well suited for leverage because investors cannot force the fund to redeem shares at NAV every day. That matters more than it first seems.

An open-end mutual fund must be ready for redemptions. If many investors want their money back, the fund may have to sell assets to meet those withdrawals. A CEF does not face that same daily pressure. If shareholders want out, they sell their shares to other investors on the exchange. The fund itself does not have to liquidate assets simply because one investor wants to leave.

This gives the manager more room to hold assets, borrow against them, and run an income strategy without worrying about daily redemptions. In bond CEFs, leverage is especially common because the fund is trying to turn interest-bearing assets into a stronger income stream. The fund borrows, then invests in longer-term bonds or credit instruments. If the difference between what the fund earns and what it pays to borrow is positive, leverage can be attractive.

That is why leverage is not merely a trick. It is one of the reasons many income-oriented CEFs exist.

The Pleasant Version

In calm markets, leverage can feel almost elegant. The fund borrows cheaply, buys more assets, collects more income, and passes a larger distribution to shareholders. The investor receives monthly or quarterly cash flow and feels that the fund is doing exactly what it promised.

And sometimes it is.

A carefully managed leveraged CEF can be a useful income tool, especially when the fund owns quality assets, borrows at a reasonable cost, keeps leverage moderate, and does not promise more income than the portfolio can realistically support. In that environment, leverage can feel like a quiet machine working in the background.

But calm markets are not permanent.

The Painful Version

Leverage becomes dangerous when the spread turns against the fund.

Imagine a fund borrows at 3% and owns bonds yielding 6%. That spread looks healthy. Now imagine short-term rates rise and the fund’s borrowing cost climbs toward 5%. At the same time, the value of the bonds falls because higher interest rates make older bonds less attractive.

The fund is hit twice. Its income spread narrows, and its asset values fall. Because the fund is leveraged, the decline in asset value is felt more sharply by common shareholders. The debt or preferred shares sit ahead of them. Losses are absorbed by the equity layer.

That is the part many new income investors miss. They see the yield, but they do not always see the balance sheet.

Leverage and Interest Rates

Interest rates are the weather system of leveraged income funds. When short-term borrowing costs are low and longer-term assets yield more, the environment can be favorable. When short-term rates rise quickly, leverage becomes less comfortable.

This is especially important because many leveraged CEFs borrow short-term and invest longer-term. That structure can work well, but it also creates rate sensitivity. The fund’s borrowing cost can adjust faster than the income from the assets it owns.

That does not mean every leveraged fund will fail when rates rise. It means the investor should ask better questions: how much leverage does the fund use, is the borrowing fixed or floating, what is the cost of leverage, how much income remains after leverage expenses, and what happens if short-term rates stay high?

Those questions matter more than the headline yield.

Leverage and NAV

Leverage also affects NAV. If the assets inside a fund rise in value, leverage can increase the gain for common shareholders. But if the assets fall, leverage can magnify the decline.

This is why a leveraged bond CEF can feel strange to a beginner. The fund may own bonds, which sound conservative. It may pay regular income, which feels comforting. But the market price can still move sharply because the fund is not simply holding bonds. It is holding bonds with borrowed money attached.

The assets may be calm. The structure may not be.

That is one of the quiet traps in income investing. A boring asset can become less boring when leverage is added.

Leverage and Discounts

Leverage also affects how the market prices CEF shares.

A leveraged fund may look attractive when borrowing costs are low and the income spread is favorable. Investors may be willing to pay closer to NAV, or even above NAV, if they believe the fund gives them access to income they could not easily create themselves.

But the opposite can also happen. When investors become nervous about leverage, the market price can fall faster than NAV. The discount can widen. A fund that looked cheap can become cheaper. A fund that already had a high distribution can suddenly look fragile.

This is why discounts in leveraged CEFs require extra care. A 12% discount is not automatically a bargain if the fund is overleveraged, exposed to weak assets, or vulnerable to higher borrowing costs.

Price matters. But structure matters first.

The Motorcycle Engine Problem

A simple way to think about leverage is this: leverage is like putting a motorcycle engine on a bicycle.

On a smooth road, it feels brilliant. You move faster. You cover more ground. You wonder why every bicycle does not have one. Then the road gets wet, and the same engine that made the ride exciting now makes every mistake more costly.

That is leverage.

It does not create discipline. It does not create judgment. It does not turn weak assets into strong ones. It only amplifies the result of the assets, the borrowing cost, and the manager’s decisions.

Good structure becomes better. Bad structure becomes worse.

A Simple Leverage Checklist

Before buying a leveraged CEF, look at five things.

First, check the leverage ratio. A fund using 20% leverage is not the same as a fund using 40% leverage. More leverage means more sensitivity to asset price declines and borrowing costs.

Second, check the type of leverage. Some funds use debt. Some use preferred shares. Some use credit facilities. Each has different costs, rules and risks.

Third, check the cost of leverage. If borrowing costs have risen, the fund may still show a high distribution, but the economics underneath may be weaker than they were a few years ago.

Fourth, check asset quality. Leverage on high-quality municipal bonds is different from leverage on lower-quality credit, emerging market debt or volatile equity strategies.

Fifth, check distribution coverage. If a fund uses leverage but still cannot cover its payout, the yield may be telling a dangerous story.

When Leverage Can Make Sense

Leverage is not always foolish.

It can make sense when the fund owns quality assets, borrows at reasonable cost, uses leverage moderately, and maintains a distribution that is supported by real income. It can also make sense for investors who understand that the market price may swing more than the assets inside the fund.

That last point is important. A leveraged CEF is not a savings account. It is not a stable cash box. It is a market-traded income vehicle with a balance sheet. The income may be attractive, but the ride can be rough.

The investor who understands this may use leverage carefully. The investor who does not understand it may confuse a high distribution with safety.

What to Avoid

Be especially careful with funds that combine several warning signs at once: high leverage, weak asset quality, a very high distribution, a declining NAV, repeated distribution cuts, or a discount that looks wide but has been wide for years.

Any one of these may be explainable. Together, they deserve caution.

The market is not always right. Sometimes it panics. Sometimes it misprices assets. Sometimes it throws good funds into the clearance aisle. But sometimes the market is simply looking at the same risks you are ignoring.

The Bottom Line

Leverage is one of the reasons Closed-End Funds can produce high income. It is also one of the reasons they can hurt investors who only look at yield.

The tool itself is not evil. Borrowing can increase income when the spread is favorable. It can allow ordinary investors to access institutional borrowing economics. It can help a fund produce more income than an unleveraged portfolio. But leverage always comes with a trade-off.

More income often means more sensitivity. More yield often means more fragility. More power often means less forgiveness.

A calm income investor does not reject every leveraged CEF. But he does not admire leverage blindly either. He looks under the hood.

Because in income investing, the danger is rarely the thing you can see on the front page. It is usually the thing hidden behind the yield.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. Investing involves risk, including the possible loss of principal. Always do your own research or consult a qualified financial professional before making investment decisions.