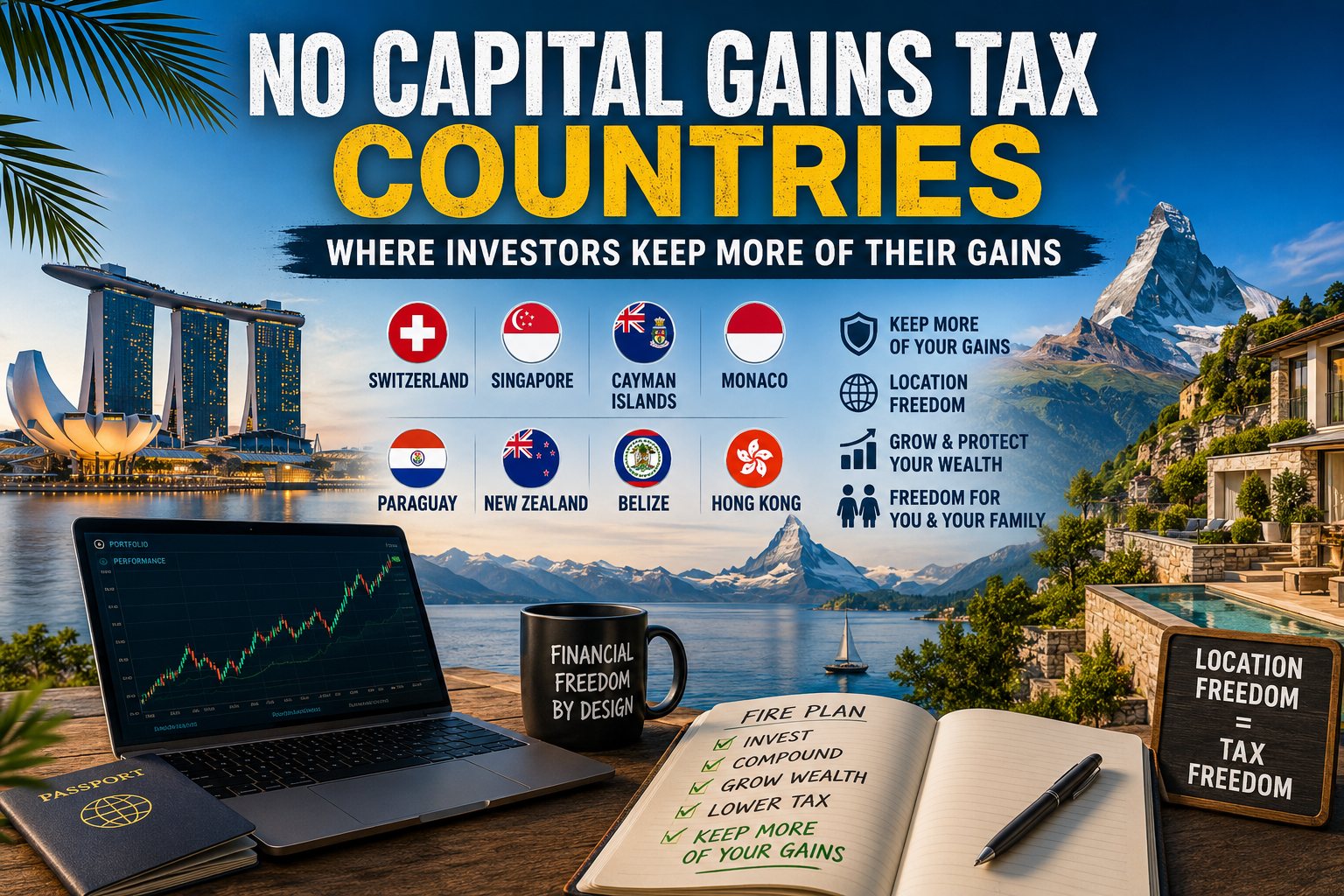

No Capital Gains Tax Countries: Where Investors Keep More of Their Gains

No Capital Gains Tax Countries: Where Investors Keep More of Their Gains

There is a quiet tax that many investors do not think about until it is too late.

Capital gains tax.

It does not usually appear when you receive your salary. It does not arrive every month like rent or a mortgage. It waits quietly in the background while your stocks rise, your business grows, your property appreciates or your crypto position finally recovers.

Then, at the moment you sell, the state appears.

That is why capital gains tax matters so much.

For ordinary savers, it may feel like a technical detail. For serious investors, entrepreneurs and FIRE families, it can change the entire outcome. A tax on gains is not just a tax on a transaction. It is a tax on compounding, patience, risk-taking and delayed gratification.

The investor takes the risk.

The state arrives for the gain.

That is why countries with no capital gains tax deserve attention.

But they also deserve caution.

A country that does not tax capital gains is not automatically the best place to live, invest or raise a family. The right question is not only, “Where can I sell without capital gains tax?” The better question is, “Where can I legally build, protect and realise gains while still living in a country that actually works?”

That distinction matters.

What Is Capital Gains Tax?

Capital gains tax is a tax on the profit you make when you sell an asset for more than you paid for it.

If you buy a stock for $10,000 and later sell it for $25,000, the $15,000 profit may be a capital gain. If you buy a rental property for €200,000 and sell it for €300,000, the €100,000 increase may be a capital gain. If you build a business and later sell it, the sale proceeds may also create a capital gain.

Different countries tax these gains in different ways.

Some tax gains heavily. Some tax only certain types of gains. Some distinguish between short-term and long-term gains. Some treat frequent trading differently from long-term investing. Some tax real estate but not listed shares. Some tax business assets but not normal private investments.

And some countries do not impose capital gains tax at all, at least for many ordinary investment gains.

That can be extremely powerful.

Why Capital Gains Tax Matters for FIRE

FIRE investors usually focus on the accumulation phase: earn well, save aggressively, invest the difference and let compounding do the work.

But eventually, the portfolio must be used.

That is where capital gains tax becomes important.

A dividend investor may pay tax on income along the way. A growth investor may defer tax for years while the portfolio compounds. But when the growth investor sells shares to fund living expenses, rebalance a portfolio, buy property, move countries or simplify holdings, capital gains tax can become a major drag.

The same applies to entrepreneurs.

A founder may spend ten years building a business. The real wealth event may happen only once: at sale. If that sale is taxed heavily, the difference between jurisdictions can be life-changing.

This is why tax residence matters before the liquidity event.

Do not wait until the gain exists.

Plan before the gain is realised.

No Capital Gains Tax Is Not Always Simple

The phrase “no capital gains tax” sounds clean.

Reality is messier.

A country may not have a general capital gains tax, but it may still tax certain gains under other rules. Real estate gains may be taxed. Business gains may be taxed. Trading income may be treated as ordinary income. Gains from professional speculation may be taxed differently from long-term private investing. Local or cantonal rules may apply. Exit taxes in your old country may matter. Controlled foreign company rules may matter if you own a company.

This is why no-CGT countries must be studied carefully.

You need to know what kind of gain you have.

Shares?

Crypto?

Real estate?

Private company sale?

Options?

Business assets?

Foreign-source gains?

Local-source gains?

A country that is excellent for one type of investor may not be excellent for another.

The Common List of Expat-Friendly No-CGT Countries

Older no-capital-gains-tax lists often included Belgium, but that is now outdated. Belgium is introducing a capital gains tax on financial assets from 2026, so for a current FireByMike version, Paraguay is a better country to discuss because of its territorial approach to foreign-source income.

That gives us a more current and practical list for globally minded investors:

Common No-Capital-Gains-Tax Jurisdictions for Investors

Switzerland Singapore Cayman Islands Monaco Paraguay New Zealand Belize Hong Kong

But the list itself is only the beginning.

The real work is understanding which country fits which investor.

The FireByMike No-CGT Test

Before getting excited about any no-capital-gains-tax jurisdiction, use a broader framework.

1. What asset are you selling? Listed shares, crypto, real estate, business equity and private assets may be treated differently.

2. Are you an investor or a trader? Some countries treat frequent trading or professional investing differently from passive long-term ownership.

3. Are gains domestic or foreign? Local real estate or business gains may be taxed even where foreign portfolio gains are not.

4. Can you legally become tax resident? A tax rule is useless if you cannot access the jurisdiction properly.

5. What did your old country tax on exit? Exit taxes, deemed disposals and anti-avoidance rules can follow you out the door.

6. Is the country livable? Banking, healthcare, safety, schools, costs and family fit still matter.

7. Are the rules stable? A tax advantage is less valuable if it depends on fragile politics or temporary incentives.

This test protects you from the classic mistake: treating a tax rule as if it were a complete strategy.

Switzerland: Stable, Sophisticated, But Not Simple

Switzerland is one of the most attractive countries in the world for wealth preservation.

It has strong institutions, excellent infrastructure, a deep banking tradition, political stability and a reputation for legal reliability. For investors, that combination matters. Tax is important, but predictability may be even more important.

Switzerland is often described as having no capital gains tax on private securities gains, but the details matter. Gains may be taxed if the person is considered to be trading professionally. Real estate gains are treated differently. Cantonal and municipal rules also matter.

So Switzerland is not a “simple tax haven.”

It is a serious jurisdiction for serious planning.

For the right family, Switzerland can be extraordinary: safe, stable, clean, efficient and globally respected. But it is expensive. Housing, healthcare, schooling, services and daily life can be costly. For a high-net-worth family, that may be acceptable. For a modest FIRE investor, it may reduce the benefit.

Switzerland is not cheap freedom.

It is premium freedom.

Singapore: Investor-Friendly, Efficient, But Tightening

Singapore is one of the world’s great financial centres.

It offers efficiency, safety, world-class infrastructure, strong banking, political stability and a deeply international business environment. For entrepreneurs and investors, it is one of the most serious jurisdictions in Asia.

Singapore generally does not impose capital gains tax on personal investments. However, the picture has become more nuanced. Certain foreign-sourced disposal gains and entity-level structures may require careful analysis, especially where companies, foreign assets or economic substance rules are involved.

That is the important lesson.

Even excellent jurisdictions change.

Singapore remains attractive, but it is not a place for lazy assumptions. The investor needs professional advice, especially when companies, foreign assets or larger structures are involved.

For family life, Singapore is safe, clean and highly functional. But it is also expensive, competitive and not necessarily easy for everyone to settle in permanently.

Singapore works best for people who value efficiency over romance.

Cayman Islands: Tax-Free, Beautiful, Expensive

The Cayman Islands are one of the clearest examples of a tax-friendly jurisdiction.

No personal income tax. No capital gains tax. A major offshore finance industry. English-speaking. Beautiful beaches. Strong international reputation in funds, banking and offshore structures.

The attraction is obvious.

But the Cayman Islands are not a budget geo-arbitrage destination. Residency can be expensive, housing costs can be high, and daily life may require significant capital. Establishing residency can be straightforward for the right investor, but the required real estate or business commitment is not small.

For wealthy investors, Cayman can be a powerful base.

For ordinary investors, it may be more useful as a symbol of what tax-free living looks like than as a realistic family plan.

The Cayman Islands are not cheap.

They are strategic.

Monaco: No CGT for the Ultra-Wealthy

Monaco is one of the world’s most famous no-tax jurisdictions.

It offers glamour, safety, prestige, Mediterranean lifestyle and strong appeal for the ultra-wealthy. Capital gains are generally not taxed for residents, unless specific exceptions apply. But Monaco is not designed for ordinary budgets.

Housing costs are extraordinary. Entry requires substantial means. The lifestyle is luxurious but narrow. For a billionaire, family office or very high-net-worth individual, Monaco may make sense. For a normal FIRE family, it is usually not geo-arbitrage. It is wealth preservation at the very top of the market.

That does not make Monaco irrelevant.

It teaches an important lesson.

The best tax jurisdiction may be unusable if the cost of access is too high.

Paraguay: Territorial Tax, Low Cost, But Still a Developing Market

Paraguay is interesting because it offers something many investors are looking for: a territorial tax system combined with relatively low living costs and accessible residency.

For globally mobile investors, the attraction is clear. Paraguay generally taxes Paraguayan-source income, while foreign-source income is usually outside the local tax net. That can make Paraguay attractive for investors whose portfolio income, capital gains, dividends or business income arise outside Paraguay. But this is not the same as saying that Paraguay never taxes capital gains. Domestic Paraguayan-source gains can still fall within the local tax system.

That distinction matters.

Paraguay is not Monaco. It is not Singapore. It is not Switzerland. It is a developing South American country with lower costs, a simpler lifestyle, more friction in infrastructure, and a very different legal and business environment.

For some investors, that is a problem.

For others, it is exactly the opportunity.

Paraguay may appeal to people who want a lower-cost base, territorial taxation, a more accessible residency route and a less expensive alternative to the classic tax havens. It can be especially interesting for investors whose wealth is built internationally rather than locally.

But the investor should be realistic. Healthcare, schooling, banking, legal reliability, language, safety, bureaucracy and family fit all require careful research. Paraguay can be useful as part of a Plan B strategy, but it should not be treated as a magic tax solution.

The right way to think about Paraguay is not:

“Zero tax paradise.”

The better way is:

“Potentially useful territorial-tax base, if your income is foreign-source and your family can actually live with the trade-offs.”

That is much more accurate.

New Zealand: Livable, Stable, Remote

New Zealand is not a traditional tax haven.

It is a stable, developed, English-speaking country with beautiful nature, strong institutions and a high quality of life. It does not have a broad capital gains tax in the usual sense, although specific rules can apply to property, short-term sales and certain investment structures.

For investors and families, New Zealand’s appeal is not only tax.

It is lifestyle, safety, distance from geopolitical centres, rule of law and family livability.

But there are trade-offs. It is remote. Housing can be expensive. Immigration access may not be simple. The economy is smaller. Travel to Europe or North America is long and costly.

New Zealand can be excellent for the right family.

But it is not a quick tax trick.

It is a lifestyle and jurisdictional choice.

Belize: Accessible, English-Speaking, But Requires Caution

Belize is attractive because it is English-speaking, relatively accessible and positioned as a lifestyle option in Central America.

Belize may appeal to investors who want lower costs, tropical lifestyle and a simpler environment than high-end offshore centres. It can also be interesting for people thinking about second residence, Central America, English-language living and a warmer climate.

But Belize requires caution.

Infrastructure, healthcare, safety, liquidity, banking and legal reliability should be studied carefully. A country can be easy to like and still difficult to use as a serious wealth base.

Belize may be more suitable as part of a broader Plan B strategy than as the only pillar of a family’s financial life.

Hong Kong: Powerful, But Politically Complicated

Hong Kong has long been one of the world’s great financial centres.

It has no capital gains tax, strong market infrastructure, an international business environment and deep financial connectivity. For decades, it was one of the clearest examples of a low-tax, high-commerce jurisdiction.

But Hong Kong also shows why tax is not enough.

Political risk matters. Rule stability matters. Personal freedom matters. The relationship with mainland China has changed the way many investors think about Hong Kong. It remains commercially powerful, but the old assumption that Hong Kong is a purely independent global hub has become more complicated.

Hong Kong may still be useful.

But it should not be treated as risk-free.

The Investor’s Real Question

The question is not simply:

“Where can I avoid capital gains tax?”

The better question is:

“Where should I legally realise gains, hold assets, live, bank and protect my family?”

Those are not always the same place.

A globally minded investor may use one jurisdiction for residency, another for banking, another for company structure, another for investment custody and another for lifestyle. That is the deeper version of geographic freedom.

Countries are tools.

Not every tool must do every job.

Capital Gains and Exit Planning

The time to think about capital gains tax is before the gain is realised.

This matters especially for entrepreneurs and investors with concentrated positions. A business sale, property sale, crypto exit or stock liquidation can trigger life-changing tax consequences.

But moving too late can fail.

Your current country may have exit tax rules. It may deem assets sold when you leave. It may continue taxing certain gains. It may treat your company as still resident. It may apply anti-avoidance rules if the move appears artificial.

This is why legal planning matters.

A tax-friendly country only helps if you can access it lawfully and at the right time.

No CGT vs Low CGT

Just as with income tax, the best answer is not always zero.

A country with low or moderate capital gains tax but excellent safety, healthcare, schools, banking, residency and lifestyle may be better than a no-CGT jurisdiction that is expensive, unstable or unsuitable.

The ideal strategy may be a balanced jurisdiction.

Not the lowest tax.

The best after-tax life.

That is why the investor should compare countries across multiple dimensions: tax, safety, rule of law, cost of living, healthcare, immigration, family fit, banking and exit options.

Capital gains tax is important.

But it is only one part of the freedom equation.

The FireByMike Capital Gains Planning Framework

Before choosing a tax-friendly country, work through the following framework.

1. Identify the gain Is it from stocks, crypto, business sale, property, funds, options or private assets?

2. Identify your current tax exposure Does your current country tax worldwide gains, apply exit tax or impose anti-avoidance rules?

3. Identify possible residency options Which countries can you legally access before the gain is realised?

4. Compare tax treatment by asset type Do not assume all gains are treated the same.

5. Check banking and investment access Can you hold assets, receive proceeds and reinvest efficiently?

6. Test livability Can your family actually live there without destroying the benefit?

7. Build exit options Rules change. Do not depend on one country forever.

This framework is less exciting than a list of tax havens.

That is why it is more useful.

The Bottom Line

Capital gains tax matters because it taxes the moment when investment finally works.

For FIRE investors, entrepreneurs and globally mobile families, reducing or avoiding capital gains tax legally can make a major difference. It can preserve compounding, protect business sale proceeds, make portfolio withdrawals more efficient and accelerate financial independence.

But no capital gains tax is not a complete life plan.

Switzerland, Singapore, Cayman Islands, Monaco, Paraguay, New Zealand, Belize and Hong Kong all offer interesting possibilities, but each comes with trade-offs. Some are expensive. Some are complex. Some are politically sensitive. Some are developing markets. Some are better for investors than families. Some are excellent for one type of gain and less useful for another.

The serious investor does not chase a headline.

He studies the structure.

The right country is not merely the one that taxes your gains least.

It is the one where your wealth, family, mobility and future are treated best.

That is the real goal.

Not tax avoidance as a lifestyle.

Freedom by design.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, legal or immigration advice. Tax laws, residency rules and capital gains treatment vary by country and personal circumstances and may change. Always consult qualified tax and legal professionals before making investment, relocation or tax residency decisions.